(Mostly) everything you need to know about Bitcoin from the last 12 months and a glimpse of what may be yet to come.

"how can bitcoin go up so much?"

Everyone wonders the same thing as they see the price of bitcoin making headlines. Some will take the time to research and buy while others will regret passively, assuming they've missed the boat entirely. Price entry after is what makes an investor successful.

The nascent Bitcoin however, makes it hard to forecast a price using traditional measures. If you take the time to understand the new paradigm, the magnitude of opportunity, and adoption that's taken place over the past 12 months, you may be left in awe. It's something you can't afford to miss.

Note: although often used interchangeably, capitalization matters - Bitcoin refers to the entire technology network, while bitcoin (₿) is the underlying currency on the network - you can think of them as the US monetary system and the dollar ($), respectively.

Most people think price when they hear about Bitcoin but there is more to this astonishing technological innovation than its purpose as a store-of-value. Bitcoin is the world's first digitally native, permissionless, global monetary network. Most of today's headlines are dominated by prices with a single bitcoin reaching trading around $50k today, so it's no surprise that people look are fascinated more with bitcoin rather than Bitcoin.

(following Bitcoin on twitter makes you appreciate memes)

The goal of this article is not to explain what Bitcoin is. Understanding the disruptive nature of Bitcoin and the technology is priceless, however, we as humans have a tendency to focus on things with a price so this article will focus on how its role as an asset has evolved over the past 12 months in an unprecedented way.

Quick Intro

Cryptocurrency seems to have come out of nowhere. In early 2017 I was introduced to Ethereum, the second largest cryptocurrency today. Having a computer science background allowed me to grasp the concept utilizing a public blockchain to maintain a distributed ledger using cryptography.

Ethereum seemed like it could be a potential replacement for money but when I applied principles of macroeconomics my conviction shifted to Bitcoin which unlike Ethereum, has a fixed supply that is artificially capped.

Fast forward through some turbulent price fluctuations to a year ago today, the world was turned upside down. COVID-19 stopped everything in its tracks. People stopped spending money and unemployment reached all-time highs. Central banks across the world responded aggressively with stimulus to keep economies afloat.

Around the time this all started, I stumbled upon Anthony Pompliano who very clearly correlated the crisis response of printing money and zero interest rates to Bitcoin. To summarize my takeaway in a few words: the aftershock of the crisis accelerated the dire need for Bitcoin by 5-10 years.

My obsession with the economic response to the pandemic and Bitcoin's role led me to realize that for the first time individuals had a head start on investing in one of the greatest innovations in history ahead of institutions - more on this shortly. With this realization last summer, I began evangelizing with my friends and family to take an interest in bitcoin.

As I started engaging with a wider audience, I was surprised at the disproportionate majority who knew little or nothing about Bitcoin besides the price it was trading at. This article intends to explain how a completely new asset class was able to 10x to a $1 trillion market cap in just 12 months and what the future may hold.

Brief History

Before getting into the trends that have developed over the past year, I'll share some history that some people may cite as a concern when considering Bitcoin: volatility. If you look at the 10 year history of the asset, price corrections are nothing new and are in fact healthy. Two of the most commonly referenced events in this regard are the correction post 2017 and the drawdown when the pandemic started in 2020 but there is a stark difference between the two.

When Bitcoin first went mainstream in 2017, it was a highly speculative asset with prominent figures like Warren Buffet calling it "rat poison squared". Nonetheless, the price went up as first time buyers piled in trying to get rich, only to later sell or trade into other cryptocurrencies which ultimately became worthless.

Right before its peak at the end of 2017, derivative bitcoin futures were introduced allowing investors to trade on margin. Futures, which are advanced investment instruments typically used by institutions, fueled the price upward but there were no (publicly announced) institutional buyers so when the price began to decline, there was a major sell-off. It was a healthy correction of market exuberance, something we've artificially suppressed with MMT as of late.

In contrast, the recent Bitcoin selloff in March at the start of the pandemic was different from 2017. It was not limited to Bitcoin. The Dow and S&P had the worst month since the Great Depression. The systemic risk of economies coming to a grinding halt caused all asset classes to plunge as markets were temporarily deleveraged and margin calls were met.

"Volatility is a feature, not a bug."

The immediate settlement of Bitcoin transactions made it the primary asset for urgent capital requirements. In the K-shaped recovery following the pandemic, Bitcoin drastically outperformed all other assets including traditional inflation hedges like gold, boasting a 200% annual return since its inception 10 years ago.

With the recent explosion in price this year, most wonder where Bitcoin will go from here. Many will look to the past corrections and stay on the sidelines until bitcoin falls below an arbitrary price. While this is a fair strategy if you have a specific thesis, it's imperative to understand why past volatility is unlikely to be a good indicator of future trends due to the paradigm shift we experienced in the past year.

If there is one thing you need to understand about Bitcoin, it's scarcity. There will only be 21 million bitcoins ever be minted. The release of this supply is performed through mining and is algorithmically controlled to decrease every 4 years through a mechanism know as halving. This deflationary characteristic is foundationally important to understand.

The objective of this article is to offer a crash course on how recent events have dramatically elevated the value of Bitcoin, both the technology and the asset representing it. While all the events are interrelated, I classify them as substantial shifts in the following three categories: (1) macro outlook (2) regulatory policies and (3) diversified demand. I will then summarize with the risks and opportunities for Bitcoin.

Macro Outlook (The Great Monetary Inflation)

The pandemic created a "black swan" event that reverberated across the globe leaving no economy untouched. The subsequent lockdowns brought everything to a halt, causing spending to go off a cliff and leaving massive unemployment in its wake. Markets got decimated and we were on the verge of a liquidity crisis that could've collapsed the international monetary system.

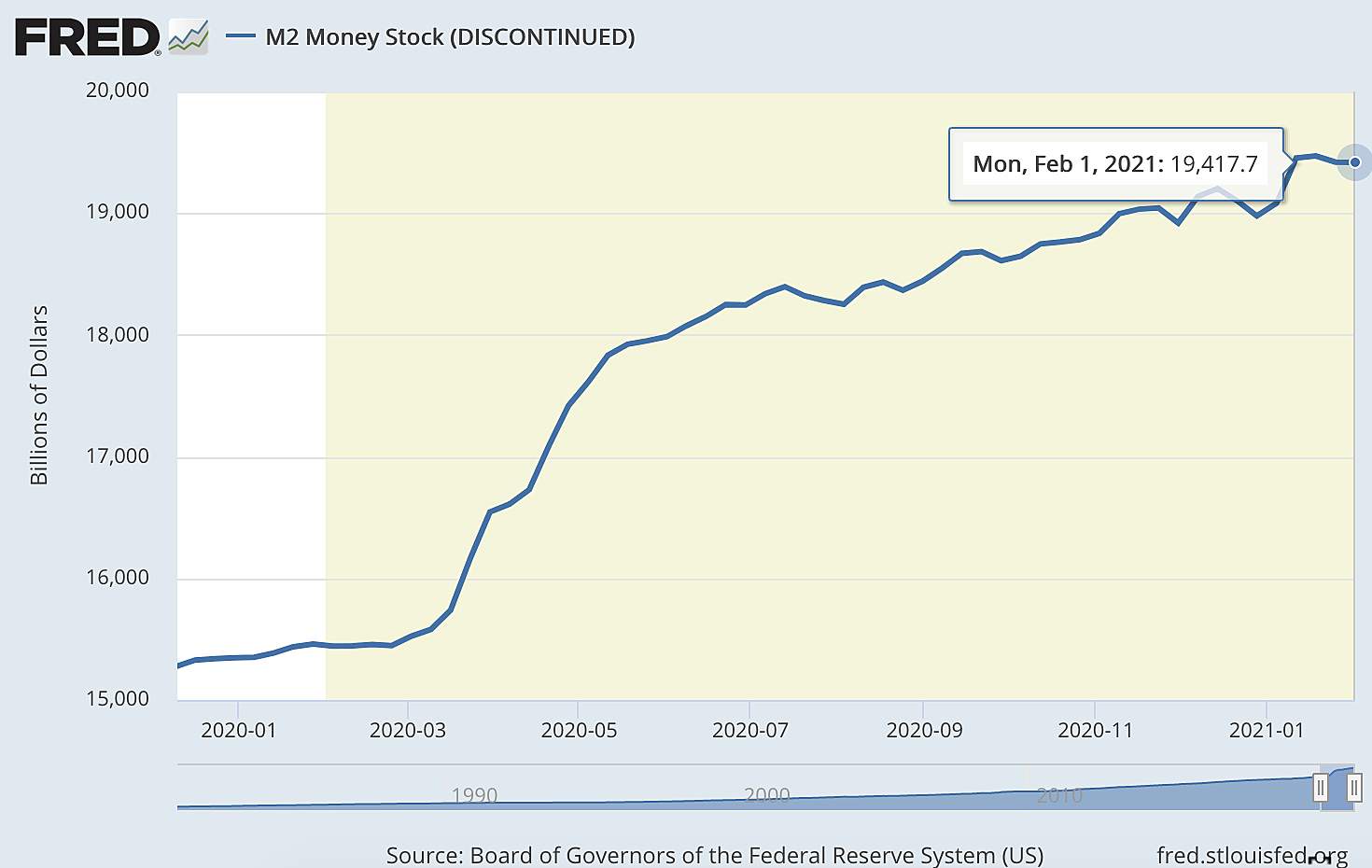

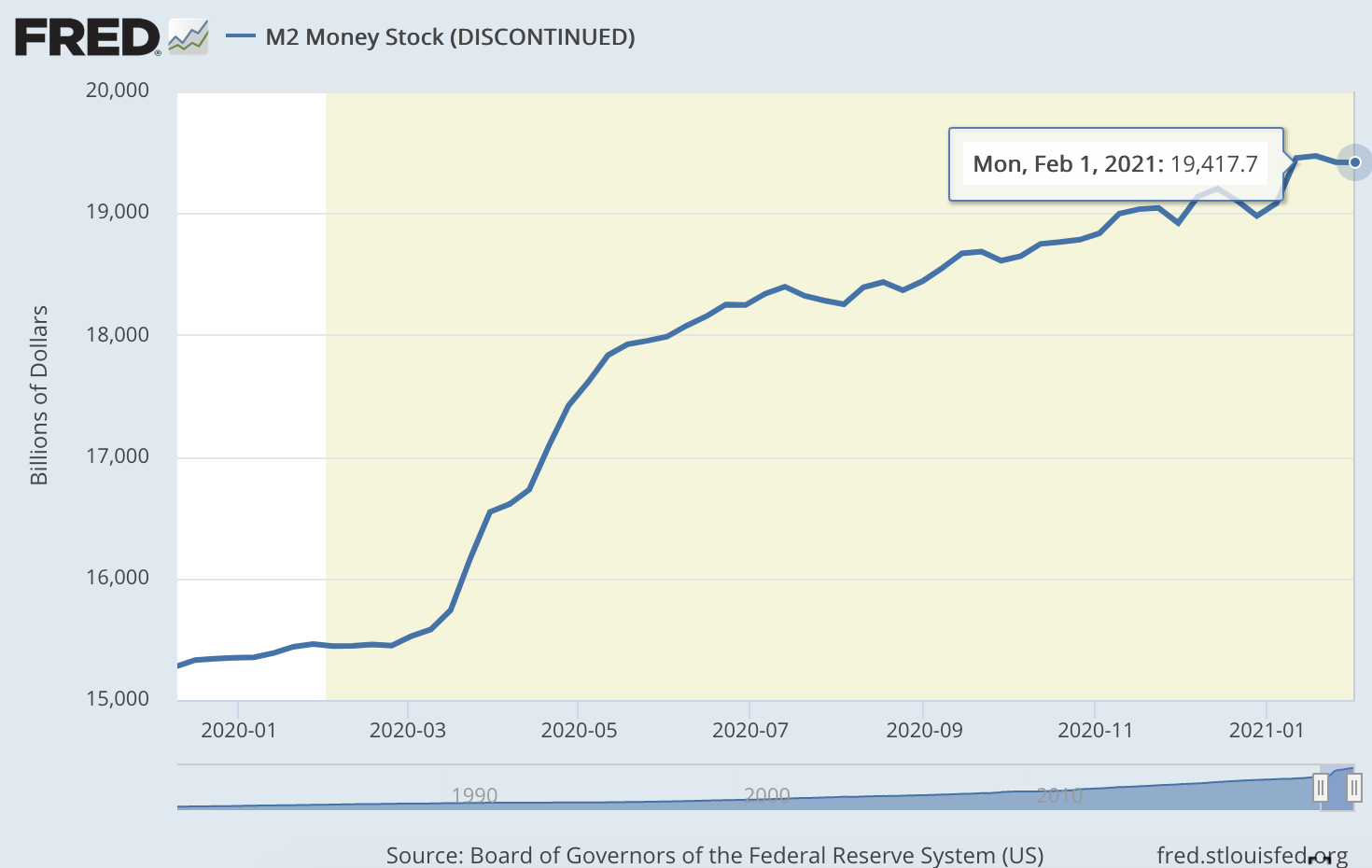

In an attempt to stop the bleeding and preventing a depression that would make 2008 look tame, central banks opted for never before seen monetary policies. Governments printed money, pumping liquidity into the system to make up for lost revenues and prop up equity markets. This happened whilst keeping rates at an all-time lows. As a result, the M2 money supply which measures the amount of dollars in circulation, increased by 28% since the pandemic started.

If the proposed $1.9T stimulus passes, that number would go up to nearly 40%. This means there will be 40% more new dollars than there were 12 months ago and there is already talk of additional infrastructure spending to the tune of $3T.

UPDATE Mar 12, 2021 - President Biden signs $1.9T stimulus package after bills passes through House and Senate along party lines.

This creation of new money is only possible because the dollar is no longer backed by anything tangible since the US dollar's convertibility into gold was suspended in 1971. Money supply is ultimately determined at the discretion of the Federal Reserve, an unelected body who's charter is to maximize employment with a 2% annual inflation target.

With the exponential rise in available money we are seeing today, it is hard to argue that we will not see inflation return in an uncontrollable fashion. Ironically, inflation was the main driver for Nixon taking us off the gold standard in 1971. Check it out 👉 www.wtfhappenedin1971.com

According to CPI we haven't seen any alarming signs of inflation just yet; it's worth noting that the official CPI metric is arguably ineffective at measuring cost of living for the bottom half of the population. The other factor impacting inflation is the velocity of money in circulation; since employment still hasn't recovered the increase in spending has not yet been factored in as far as prices are concerned.

What's undeniable is that the dollar is projected to have decreased buying power in the near future. This inadvertently forces investors to seek a cash alternative to preserve wealth, while leaving fixed and low income households in a struggle to maintain an adequate living.

Gold which has historically served as a hedge in times of economic uncertainty, surpassed $2k last last summer but has fallen substantially since. Stan Druckenmiller, known for breaking the Bank of England in 1992 (and making over $1B in the process), has publicly predicted that Bitcoin will outperform gold. Cathie Wood of Ark Invest, one of the most successful firms of the past several years agrees when it comes to the digital gold prospect.

Note the inverse price correlation between the two assets over the last 6 months in the charts above - it's not unreasonable to think that the reason Bitcoin is outperforming gold is because they are competing for the same capital, and outflows from gold are making their way into Bitcoin.

Bitcoin currently represents only 10% of gold's approximate $10T market cap so achieving the same value means bitcoin would have to 10x from today's price. This sounds unrealistic until you look at the advantages Bitcoin has as future gold 2.0.

The ease of bitcoin acquisition and custody, not having to blindly trust institutions for ownership, superb divisibility, and ability to send it across the world almost instantly makes the digital asset superior in almost every way. Bitcoin operates on a public distributed ledger so whether you hold your cryptographic keys in your pocket, on a software wallet, or keep them on an exchange you can be 100% certain that you are the undisputed owner of your bitcoin.

Regulation (The Trojan Horse)

In addition to concerns stemming from the macroeconomic policies employed by central banks across the globe, there were changes happening behind the scenes at a regulatory level. Most of these announcements flew under the radar but these changes had substantial impact on the influx of players in the crypto space.

Last May, Brian Brooks took the lead role at one of the most important regulatory bodies in the financial industry, the Office of Comptroller of the Currency. Brooks, the former Chief Legal Officer for Coinbase (set to IPO at $100B valuation), was charged with supervising all national banks and federal savings associations as head of the OCC. He was nothing short of instrumental in creating the most innovation-forward guidance for banks in his few months in office under the Trump administration.

In July 2020, the OCC released an interpretive letter clarifying the banks' ability to custody digital assets, including cryptographic keys that represent cryptocurrencies, including bitcoin. This monumental guidance eliminated the uncertainty around the nascent digital asset class, giving banks the ability to hold digital currencies such as bitcoin on behalf of their customers.

In September, the OCC issued groundbreaking guidance regarding stablecoins. Stablecoins are cryptocurrencies that are pegged to USD 1:1, essentially providing a digital version of the dollar. You may be thinking to yourself, the dollar has been digital forever. While it's true that electronic payments have become ubiquitous, the process is just an abstraction used by banks to authorize or deny a transaction.

In the case of a credit or debit card purchase, a transfer of funds doesn't actually occur at the time you swipe your card. A payment processor like VISA sends a series of messages to the issuing bank. Payments can take several days to complete as centralized ledgers among the banks need to be reconciled to finalize the transaction.

A stablecoin is a cryptographic representation of the dollar managed on a public ledger, akin to digital cash. You can hold it in your pocket (on a hardware wallet) or make a purchase using it without needing a traditional bank to facilitate the transaction, which finalizes almost instantly.

The guidance from the OCC legitimized such stablecoin activity. This was critical for two reasons. The governance ensured that reserve accounts of stablecoin issuers will be offered the same federal protections as any other depositor.

The importance of this is exemplified through the unfair treatment recently made known in the Tether fiasco where Wells Fargo abruptly ended its relationship with the stablecoin issuer, spurring NY Attorney General's investigation of fraud.

Stablecoins are also helpful due to their ability to eliminate limitations and delays that companies face when clearing funds using legacy methods. Without having to rely on traditional banks, companies could exponentially decrease transaction times.

In November, Brooks announced a new application process for national bank charters, creating a clear path for companies to become first tier money handlers. This allowed Anchorage to apply for status, and eventually become the first national crypto bank at the start of this year.

If that wasn't enough to spur innovation and momentum, the OCC multiplied the impact of its previous governance by issuing final guidance in January of this year. Through its announcement, the OCC cauterized the ability for banks to use decentralized blockchains and stablechain networks to facilitate payments transactions similar to SWIFT, ACH and FedWire.

UPDATE Mar 30, 2021 - VISA becomes the first payment processor to announce payment settlement in stablecoins, per guidance from the OCC earlier this year - link

This breakthrough helps financial institutions tackle one of the greatest challenges in the world of banking: payment settlement. What better to illustrate the importance improving our payment rails than the recent outage days ago that disrupted systems responsible for clearing TRILLIONS of dollars of transactions every day. The decentralized Bitcoin network has a better uptime record than the backbone of the US banking system. Serendipity.

(Sen. Cynthia Lummis, WY updates her twitter profile picture to laser eyes in support of Bitcoin)

Senator Lummis of Wyoming is a strong advocate for Bitcoin and financial innovation. Lummis originally bought bitcoin back in 2013 when after being introduced by her son-in-law. In her home state, she helped build out a cutting edge legal framework for digital assets. This work led to the country's first (state) crypto bank when Kraken was granted a charter in September of last year.

On February 3, Lummis was appointed to the committee responsible for the nation's financial regulation, the Senate Banking Committee. The speed at which she was able to create rails for banking requirements in her state made her an obvious pick at the federal level. Legislation is coming and it looks to be favorable for financial innovation.

Demand Diversification (The Elephant in the Room)

Past bitcoin bull markets were primarily driven by retail investors. These investors were primarily technologists who understood the underlying technology, traders who saw the arbitrage opportunity, folks looking for protection against inflation, or a combination of the above. Apart for crypto native firms, there weren't many institutional holders of bitcoin that made their holdings publicly known.

The lack of precedent and regulatory uncertainty with these new class of digital assets made it difficult for institutions to invest without taking on incredible risk to their reputations. As a result of this, your average joe has been front-running banks and other primary capital allocators, in what is shaping to be the greatest innovation since the internet. Albeit the opportunity didn't come without risk that it would all go to zero, but that is no longer seems to be the case.

“The best profit-maximizing strategy is to own the fastest horse." - PTJ

That institutional risk appetite changed in 2020 after markets were shaken and then stirred with monetary policy. In May, billionaire hedge fund manager Paul Tudor Jones announced exposure to Bitcoin through futures. In his memo about The Great Monetary Inflation he noted that “the best profit-maximizing strategy is to own the fastest horse, my bet is it will be Bitcoin”.

While this was a bullish news for Bitcoin, we still hadn't seen any money put towards Bitcoin in the public markets. That changed when MicroStrategy, a publicly traded company (NYSE:MSTR) announced that they adopted bitcoin as their treasury reserve asset by purchasing 38,250 bitcoin for ~$425M (worth over $2B today). This marked the beginning of would become a waterfall of public announcements in the space.

Fintech darling Square, soon after announced that they'd put $50M of bitcoin on their balance sheet but perhaps more importantly, they open-sourced the process to allow other companies to follow suit while minimizing regulatory risk. PayPal subsequently joined Square's CashApp by enabling their >350M users to purchase bitcoin directly through their platform, eliminating friction required to get exposure to the asset. They had a technology-first approach to financial services, so the opportunity to become an onramp to one of the greatest disruptions of the century was obvious.

UPDATE March 30, 2021 - PayPal has started allowing U.S. consumers to use their cryptocurrency holdings to pay 29 million of its online merchants globally - link

Bitcoin has penetrated pop culture as well. Many hip hop artist including 50 Cent and Snoop Dogg have publicly promoted Bitcoin. Jay-Z has even partnered with Jack Dorsey, in donating $24M to help develop the Bitcoin network through an irrevocable trust. NFL pro-bowler and Superbowl champion Russell Okung, become the first player to get paid in bitcoin. Half of his $13M dollar salary is being paid in Bitcoin earning him multiplicative bonus since the contract when into effect in last year.

In December, investor MassMutual entered the scene from a new financial sector. Insurance is one of the strictest financial industries when it comes to investments practices due to its has fiduciary responsibility of paying out claims and annuities. MassMutual, a 170-year hardened veteran dealing with investment grade products, put $100M bitcoin into its general account. The significance of this was not only that it gave credence to the asset but essentially derisking the decision for money managers in the conservative sector like pension funds to allocate a fraction of its $30T of international holdings into the deflationary asset.

(Some speculate that it was Michael Saylor of MicroStrategy who convinced Elon to purchase bitcoin with the tweet exchange from December)

On February 3, MircoStrategy held a Bitcoin for Corporations conference with thousands of companies attending to learn how to incorporate Bitcoin into their companies' financial profile. During the conference, Ross Stevens stated that he expects $25B in new money to enter Bitcoin through his firm Stone Ridge. If there was any takeaway from the speakers and attendees at the conference, it was that Bitcoin has gone from a contrarian to consensus trade albeit there weren't many investment decision were publicly revealed at that time.

Then on February 8, arguably the biggest Bitcoin announcement to date came from one of the largest companies in the world. Elon Musk announced that Tesla had purchased $1.5B worth of Bitcoin, representing an approximate 7% conversion of Telsa's cash position into Bitcoin. Accompanying the announcement were details that they planned to allow customers to purchase cars using the cryptocurrency.

UPDATE March 24, 2021 - Telsa allows purchase of cars using bitcoin and says it will not convert the earnings from sales into dollars; company is now running nodes that help secure the network - link

The Telsa purchase helped push Bitcoin past a $1 trillion market cap making it an unavoidable consideration. All major banks which have done everything in their ability to discredit and dismiss Bitcoin have been left without exposure, and now have to address the elephant in the room. Many corporations and institutions have probably already made investment decisions on Bitcoin, but execution takes time in order to comply with governance and regulations and so this year should be an exciting one. Slowly, then all at once.

Bitcoin is even getting traction from governments and elected officials. Mayor of Miami, Francis Suarez has been a vocal advocate of Bitcoin, even posting the bitcoin whitepaper to the city's website. Using twitter to broadcast his message of an innovative and business friendly domicile, the mayor has successfully attracted some of the most prominent capital allocators and technology masterminds to his city.

On February 11, Miami announced plans to allow city officials to get paid in Bitcoin and residents to pay taxes using the cryptocurrency. While actions at a municipal level may not seem ground-breaking, it is monumental for Bitcoin for two reasons: (1) acceptance as payment of taxes is viewed as a keystone qualification as money and (2) the city is creating a precent for others to follow, even at the state level. The impact of Bitcoin adoption on the city's ability to attract founders and capital makes it all the more appealing for other city and state officials to follow suit.

UPDATE March 24, 2021 - Mayor of Jackson TN is exploring ways that he can offer cryptocurrency-based payroll conversions for city employees - link

Risks

With all this activity recently you many be wondering, what does the future of Bitcoin hold? The momentum is undeniably optimistic but it's tough to say with certainty.

Despite its remarkable rise to the forefront, the nascent Bitcoin is only 11 years old. There still is some uncertainty when it comes to the new monetary paradigm. Bitcoin is essentially software that uses cryptography. The open source software is developed and maintained by the community and deployed through obtaining a consensus of the network. While it is possible that a bug is introduced into the system which compromises its integrity or security, its 100% track record indicates that it's unlikely especially when scrutiny from the rapidly expanding developer community continues to grow.

Throughout its entire existence, there have been no incidents that have undermined Bitcoin's ability to serve as a distributed ledger and payment network. With all transactions being public, trust in the network is undisputed and payment finality is almost instant. The network algorithmically prevents the double spend problem. Double spend could theoretically be initiated by a 51% attack, but that would require coordination of over 50% of the total hashrate, or computing power that serves the Bitcoin network.

One would not be able to purchase enough synthetic, or on-demand hashrate to fulfill a 51% attack. In order to assuredly carry out the attack, physical computing power would have to be generated. The complexities of purchasing and deploying the hardware to facilitate such an attack would be nothing short of a miracle due to the cost and sophistication required to coordinate, but also because it would require addressing the world wide supply shortage of necessary hardware.

The other major concern about Bitcoin coming from pundits is government intervention. While this is the topic that I spend most time thinking about, it's important to note that it is impossible to ban Bitcoin.

The private keys to a Bitcoin wallet, which can amount to billions of dollars, can be stored in your head with a seed phrase. The seed phrase is essentially a 12 word password that is used by a cryptographic hash function to generate the private keys that represent your wallet. It can be memorized and used to retrieve your bitcoin anywhere around the world with an internet connection. This makes it impossible to confiscate. Furthermore, a private key is arguably protected as intellectual property and the right to free speech, but I digress.

One thing governments can do is create highly restrictive regulation that makes wide scale adoption a challenge. This regulation would likely be imposed with major onramps such as exchanges. We had seen a lot of regulatory trailblazing already take place. Coinbase, the largest cryptocurrency exchange in the US is going public in the next several weeks paving the wave for other crypto native companies. Any draconian restrictions are unlikely as the rapid adoption continuously makes opposition politically detrimental.

Outlook

One of the primary factors in the price evaluation of any asset is its supply, and Bitcoin's will continue to rapidly decelerate until all 21 million bitcoin are minted around the year 2140. The latest Bitcoin halving occurred last May. This means that we will see half the amount of bitcoin come into circulation over the next four years as we did the last. This reduction in supply comes at a time when demand is increasing at overwhelming rate due to institutional involvement and decreased willingness to sell. The resulting price is a product of the purest form of supply and demand.

Humans are attracted by prices but traditional measures of valuation do not exist for a non-revenue generating asset class which is not tethered to a specific nation's economic output. Bitcoin has seen incomprehensibly rapid growth from $100 billion about a year ago to a market capitalization hovering around $1 trillion today. With this blazing growth, a near term doubling may seem egregious, but understanding its potential for disruption and unprecedented adoption will make you think otherwise.

Last year, Ark Invest released a white paper highlighting the largest market opportunities for Bitcoin. Among them are a global settlement network, protection against seizure, digital gold, and currency demonetization in emerging markets. The 28 page report does a fantastic job detailing these rising trends which would each accrue at least $1 trillion in additional market capitalization. Keep in mind gold's market cap is around $10 trillion.

The great financial crisis of 2008 and pandemic of 2020 have show us systemic risk in the underpinnings of the traditional financial system. My goal is not to convince you of a Bitcoin price prediction (take a look at Ark's whitepaper or the widely popular stock-to-flow model for that). My goal is make you realize the asymmetric upside potential if adoption of this new paradigm continues on the current trajectory.

how can bitcoin go up so much?

I hope the answer to the question above is a little more clear to you now. If you are wondering how to proceed, the following are sensible steps: (1) ask any questions that'll give you a comfortable understanding of Bitcoin (2) put at least x% of your savings or company's balance sheet into it (3) continue learning about Bitcoin and adjust x accordingly. There is a shift happening and it happening rapidly. Don't tell yourself you've missed it.

---

This article covers just a few keystone events that have triggered a massive shift. The ongoing announcements and headlines have accelerated since and it's incredibly exciting to follow. If all of this information was overwhelming please check out this list of readings that I've found to be very beneficial. If you have any feedback or questions feel free to reach out to me at baltaz@hey.com.