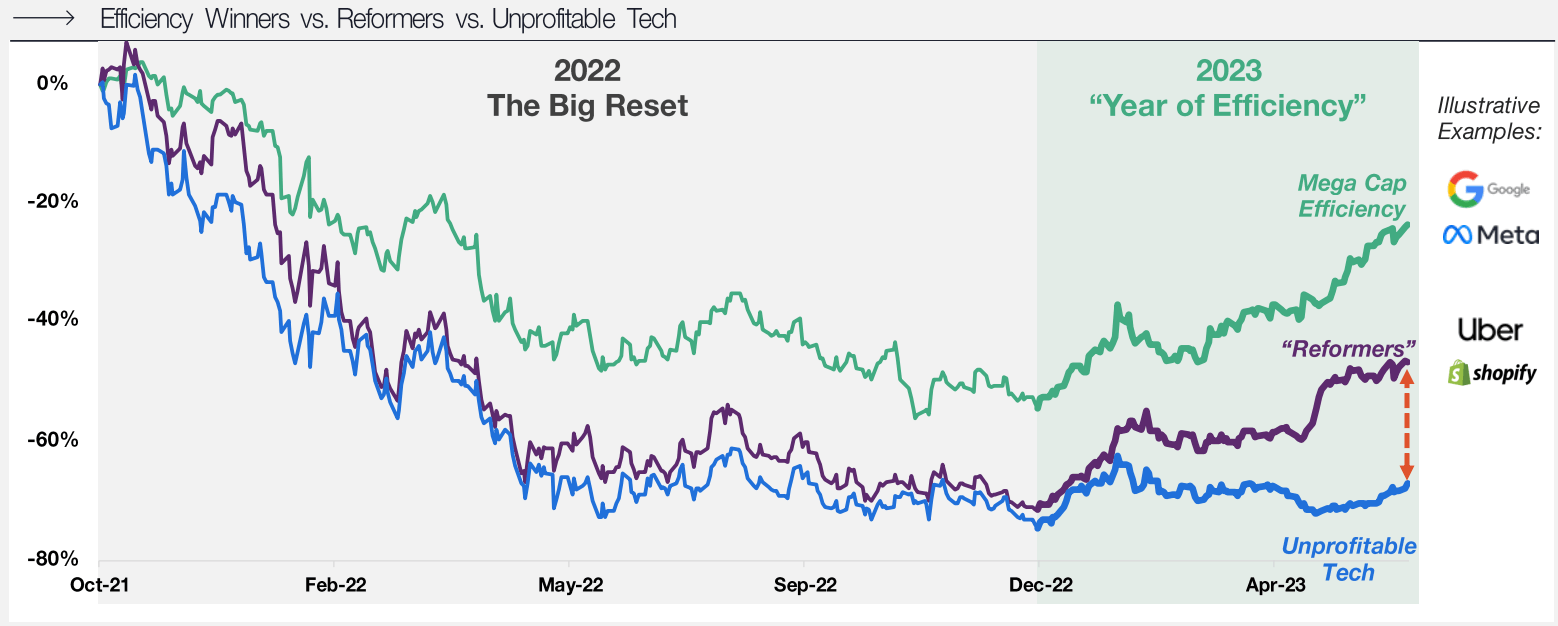

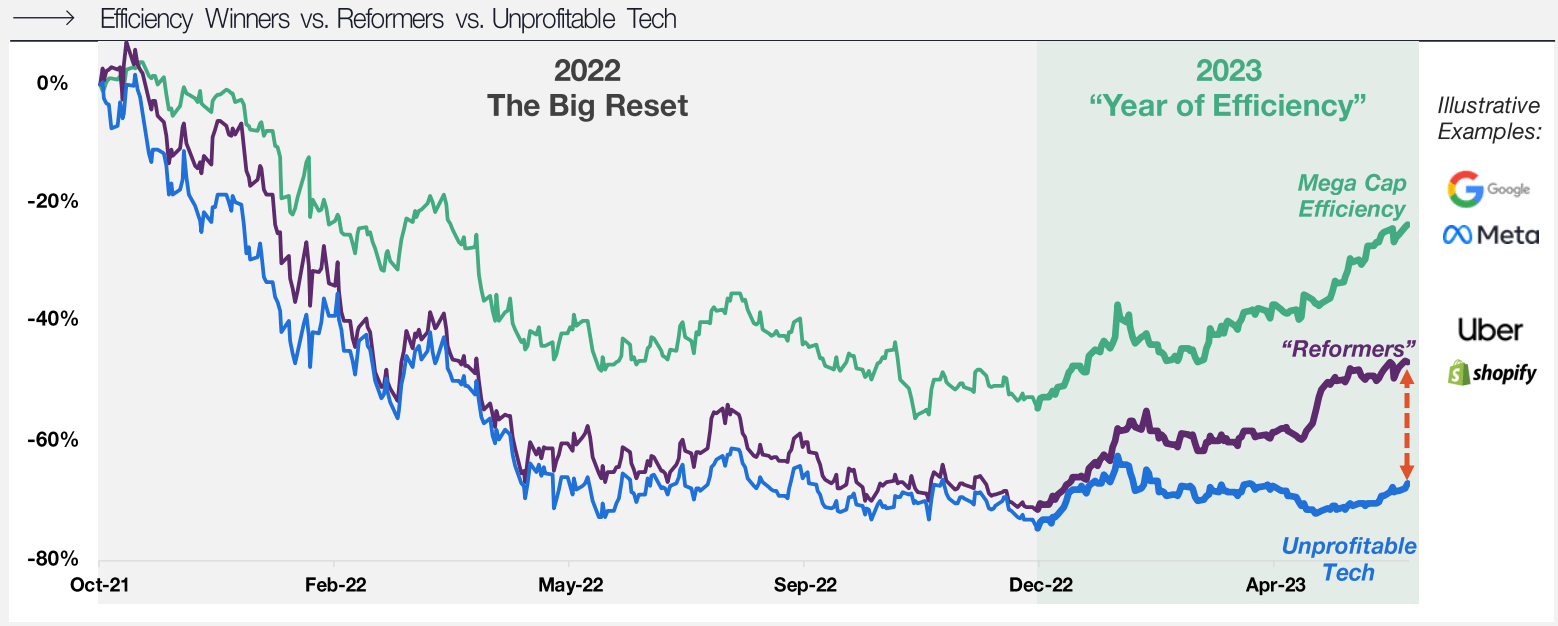

Anyone reviewing their S&P 500 retirement fund these days will do so with a broader smile than last year. The market as a whole is up, and if you're in the whole market, you're benefitting. But all of that upside, basically, belongs to just a handful of mega tech companies.

This is not a general turn-around, and it's barely a turn-around at all for the unprofitable SaaS companies that saw their bubble burst last year. In software, only cash spigots like Apple and Microsoft are able to set fresh all-time highs. Investors who bought into money pits like Asana, Monday, or Smartsheet are still likely to be in despair over their evaporated values.

This is an important change from the marathon bull run that lifted all tech businesses, no matter how unprofitable or far-fetched, in the time from the Great Recession and until the peak at the end of 2021. We're now back in world where the actual business metrics and mechanics of individual operations determine the value assigned to their stocks and startups.

But it also means that there's probably a lot more pain in the pipeline for unprofitable software startups, almost all of which are now SaaS, which raised money in the late go-go days. If a company raised a wallop of cash in 2021, they're soon coming up on that 18-month anniversary when it's supposed to be all spent. Now that runway has likely been extended by early cost-cutting, but those cuts won't last forever, and when fresh capital is inevitable needed, it'll be murder on the cap tables. Potential victims here include ClickUp, Airtable, and Notion. All who raised hundreds of millions at the peak of the market at insane valuations that'll be extremely difficult to live up to.

But it's true that you can indeed continue to run a loss-making tech company for an impressively long time, once it's sucked in enough investment capital or exists in the public markets. Groupon, for example, was once valued at a staggering $25 billion. Now their market capitalization is down to $200m, and they're warning about the risks to being "an ongoing return", but the doors are still open – twelve years after they went public!

Point being that, at a large enough scale, there's substantial lag between the infliction of a mortal financial wound and the final burial of the bleeding company. But you'd be silly, as an investor, employee, or customer, not to pay attention to the red drain once it's begun.

Unless there's a sudden, swift turn-around in investor sentiments, and nothing is currently pointing to that for unprofitable enterprise SaaS in particular, I don't think we've seen anything yet. It's a truism that if you bleed long enough, you will eventually die, though, and boy has there been a lot of bleeding already!