Time Magazine called them the "World's Most Comfortable Shoes."

The company raised $348 million with its IPO.

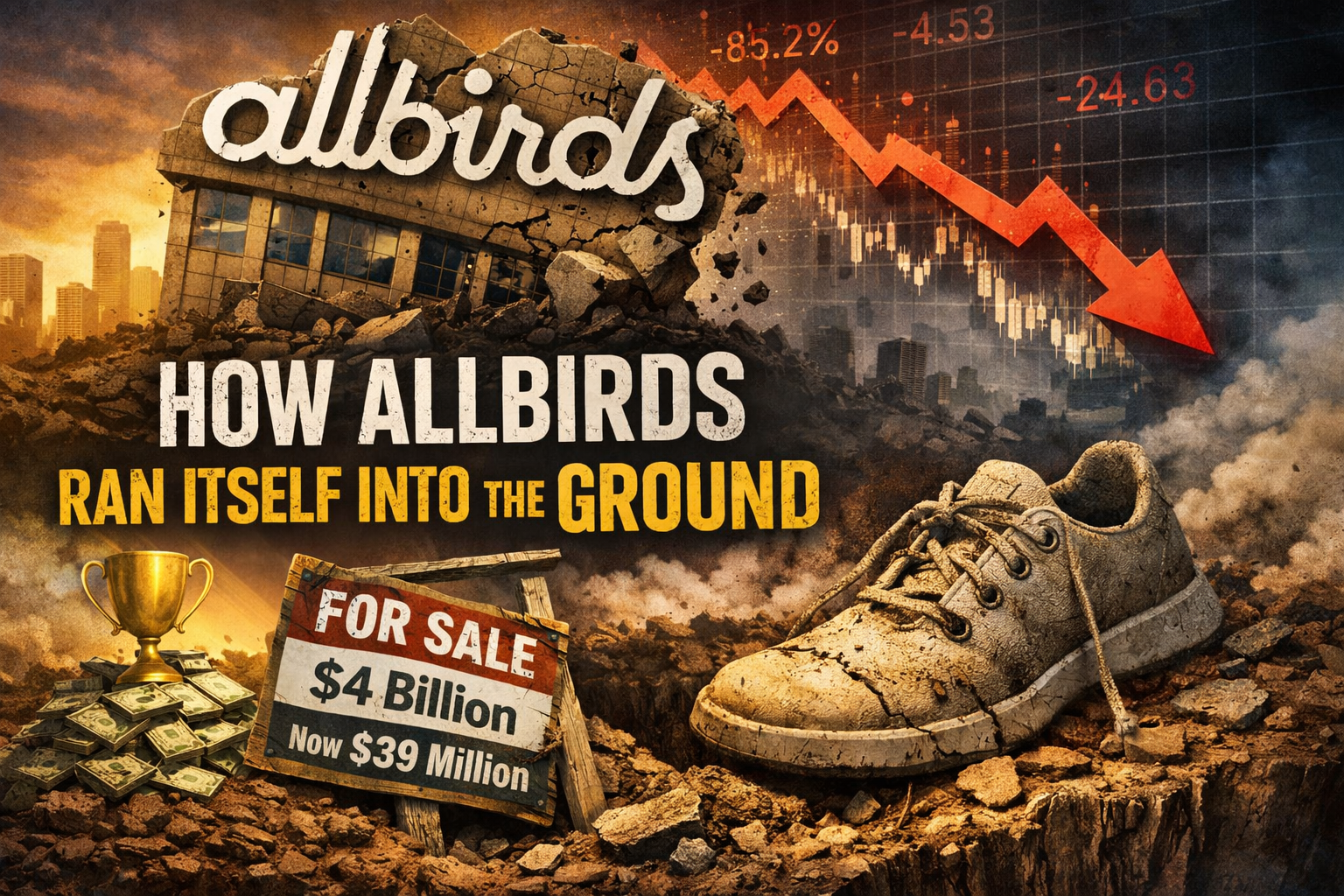

At its peak, the company was worth just shy of $4 billion.

$39 million. That's what Allbirds sold for this week.

Image created by chatGPT

The headlines say that Allbirds failed because consumer interest for sustainability is waning.

That narrative is wrong. Allbirds didn't collapse because sustainability went out of fashion, and it didn't collapse because the shoes were bad.

Sustainability In Every Step with Materials From The Earth

That’s what they set out to deliver.

The original Wool Runner shoe was genuinely novel: merino wool upper, sugarcane-based sole, comfortable beyond belief.

Barack Obama wore them. Leonardo DiCaprio invested. In 2017, the New York Times called them the Silicon Valley uniform as if that’s real traction, but it was clearly a product people actually wanted.

The product was good. The mission was coherent. The early growth was fast and organic.

And then they took the VC growth playbook seriously.

Go big

Allbirds went public (IPO) on 3 November 2021, priced at $15 a share. It opened at $27.55. This was the absolute peak of the direct-to-consumer valuation mania, a moment when mission-driven consumer brands were trading at 12-16x revenue multiples before the market had tested whether any of them could sustain.

Allbirds had never turned a profit. It didn't matter. The story was good enough during that zeitgeist.

Maveron, the VC firm co-founded by Starbucks legend Howard Schultz, that led Allbirds' Series A (total $7.25 million), saw its stake reach a whopping $399.3 million.

Unusually, neither the founders nor Maveron cashed out during this moment of liquidity. Which makes the rest of the story even more bizarre. They must have really believed that they could raise the valuation even further.

Go big or go home

Public company life however requires a public company response. Once trading on NASDAQ, Allbirds couldn't quietly grow at 20% a year and call it good. Institutional shareholders needed the revenue line to move aggressively.

By late 2023, Allbirds had 45 US retail stores. They were too large for the product range. As then-CEO Joe Vernachio later admitted, the stores were "too large for its need, not allowing for an enticing display of its shoes."

The company expanded into performance running with the Tree Flyer sneaker in 2022, aimed at younger customers and a bigger audience.

Allbirds core shoes sat at $120–160, a premium that held when the product felt singular. But when they expanded into performance running, they were asking customers to pay competitors prices for a brand without any athletic credibility. The sustainability premium doesn't travel well into categories where performance is the purchase driver.

It launched wool leggings and puffer jackets. None of which connected to the core customer: the 30s and 40s lifestyle buyer who'd fallen for a simple, well-made wool sneaker.

Sound familiar? A brand that works, suddenly stretched into shapes it was never meant to take, in order to fulfil promises it couldn’t keep.

The delay on wholesale distribution was equally damaging. Allbirds had bet on direct-to-consumer exclusivity: online sales, no middlemen, total brand control, highest margin.

When it finally pursued retailers Nordstrom and REI in 2022, the brand had already peaked. The customer acquisition economics that had made the direct-to-consumer model look clean in 2016 were long gone.

Digital advertising costs on Facebook and Google rose sharply from 2020 onwards, a trend widely reported across the industry. Without wholesale distribution, Allbirds had to keep feeding the ad machine to find new customers. The unit economics were never going to work.

Then Apple's iOS 14.5 update in April 2021 gutted the Facebook targeting that DTC brands had built their acquisition models on and Allbirds, with no wholesale safety net, had nowhere to hide.

Inevitable, or not, you decide

Two similar companies show what a different choice looks like:

On Running, the Swiss performance shoe brand, IPO'd in September 2021. The same moment, the same market conditions, the same access to capital. Roger Federer was an investor and ambassador. On Running stayed in its lane, performance running, wholesale-first, clear identity. By 2024, revenue had reached $2.5 billion. They knew who they were selling to and they didn't dilute it.

Patagonia is the starker contrast. In 2022, founder Yvon Chouinard gave the entire company to a charitable trust specifically to avoid the pressure of a public market exit. He looked at what the IPO path does to mission-driven brands and chose differently. Patagonia remains profitable, coherent, brand still intact and protected for life.

The end in sight

Tim Brown stepped down as co-CEO in May 2023. Joey Zwillinger followed in March 2024. Both were present for every post-IPO decision. Both were vocal about the brand's potential throughout.

Tim Brown, put it plainly in 2025: "With the rapid success that came our way, we lost some of our DNA."

“Rapid success.” That's the polite phrase for what VC funding and public market pressure does to a brand that was working.

The Fortune headline from August 2025: "Allbirds revenue has plummeted, but it says it has a plan."

The plan: Firesale

In January 2026, all remaining full-price Allbirds stores in the US closed.

In March 2026, the company signed a definitive asset purchase agreement with American Exchange Group, a private brand management firm whose portfolio includes Ed Hardy and Aerosoles, for $39 million. The deal covers intellectual property and certain assets. American Exchange Group isn't buying the business. They're buying the name and the intellectual property. That's their model: distressed or legacy brands, managed as IP.

Someone built something genuinely good, and then five years after the IPO, there is no Allbirds company. The IP ended up as a line item in a brand licensing portfolio.

I don't think Allbirds was unique in being badly managed. The founders were smart people who'd built something real. But the moment they accepted institutional capital at a growth-stage valuation, the company's survival depended on becoming something it wasn't.

The IPO compressed that timeline into a sprint. The decisions that followed, the stores, the product sprawl, the delayed wholesale, might seem like reckless gambles but in reality, they were rational desperate responses to the pressure of a $3.5 billion market cap that required growth at all costs.

Given that the founders and initial investors never financially exited or cashed out, I can’t help but wonder what would it have looked like if they'd stayed private, grown slowly, and protected what made the product worth caring about in the first place?

The end result really couldn’t have been worse.