[For a more detailed understanding of Bitcoin and what it means for our current financial system, read The Bitcoin Standard by Saifedean Ammous]

Until quite recently, I viewed Bitcoin simply as a new, more efficient way to make and receive payments.

I'd heard about the limited number of Bitcoins and how its supply couldn't be inflated. However, since I'd learned economics from Yanis Varoufakis (heavily influenced by John Maynard Keynes), I was always sceptical of Bitcoin being useful for mass adoption.

The downside of trusting experts is that you never truly understand what they're telling you.

Keynesian Economics

In short, Varoufakis (via Keynes) had me believe that without the ability to inject new 'liquidity' into the economy i.e. print more money, the money supply would not be fit for purpose.

The Keynesian economist relies on the following axiom:

Aggregate expenditure is equal to aggregate income.

Not spending is essentially bad because (according to Keynes) it means less income for the economy. "Austerity" therefore doesn't work because it cripples the economy just when it needs spending the most.

It takes into account game theory, where participants notice that others aren't spending, and therefore withhold their cash. When this happens, there is no liquidity (cash) in the economy to keep trade moving and so everything grinds to a halt - until and unless someone makes the first move and starts spending again.

However, where Keynesians fall short is in their solution to this 'problem.' They suggest we should spend our way out of it, regardless of economic cycles, through government intervention and an increased money supply.

In reality, stopping spending (periodically) is a good thing. It shows that the market value of goods is over-priced and that resources have been misallocated. More on this in a moment...

2008 Financial Crisis

Let's take the post-2008 financial crisis as an example, when the housing bubble burst. Banks had gotten involved in unmitigated lending, with money they did not have, to people who were at a high risk of defaulting on their mortgages.

When the bubble burst and people couldn't pay back their loans, not only did people lose their homes, but banks couldn't cover their own obligations, which led to a financial collapse.

What caused this in the first place was the ability for banks to create enormous amounts of debt (money) out of thin air. The only reason they could do this was the backing of a lender of last resort, the central bank - essentially a government-controlled entity.

If the banks had not been given carte blanche by the government central banks, they would have been far more careful about lending to people. Too many defaults and those banks would've had to close down, so they would've been much less likely to engage in irresponsible lending.

By eliminating the risk of defaults from irresponsible lending, the government (via the central banks) are essentially choosing what we ALL spend our money on.

This goes for every industry that the government funds, which becomes 'too big to fail.' If the government backs it, then it doesn't matter how bad the investments perform, or how overpriced they become, because the money supply to those investments is practically unlimited. The people who pay for those investments are all of us, in the form of a higher cost of living due to inflation.

To the average citizen, this all seems pretty normal. The government decides what industries can't fail (banking in this instance) and their money supply is limitless.

But what happens when all the money that's being pumped into an industry doesn't come good? Not only is the money wasted; it also 'wastes' other truly productive forms of human effort that would have developed further had all the attention and money not been focused on the government-directed investments.

So, to come back to my earlier point, and Varoufakis' error: by continuing to spend regardless of a natural reset (or recession) that takes place after bubbles burst, we actually short-circuit the ability for people to begin 'choosing' what is truly useful to them and what is not, and allow the price of the good to reflect that.

For example, if people realise they aren't going to get a mortgage they can't afford, they aren't going to focus on it, and they will think of other ways to improve their living standards and/or make investment returns. This would allow house prices to drop to a level that the market (people) are comfortable paying, without government intervention.

Government Spending and Real Estate

Government spending and monetary policies such as quantitative easing (printing money for failed banks), low-interest rates, and various housing incentives have significantly boosted investments in real estate.

While real estate is an important utility, and can even offer rental incomes, government support has inflated its attractiveness compared to other asset classes.

As a result, people tend to invest in real estate over other productive assets, such as equities in companies that could be developing innovative products and services and/or making the ones we already have more efficient and therefore cost effective.

Most essential products and services become cheaper with increased investment due to economies of scale and improved efficiencies. Ideally, housing prices should also become more affordable with investment, but government policies inflate demand and prevent true market corrections.

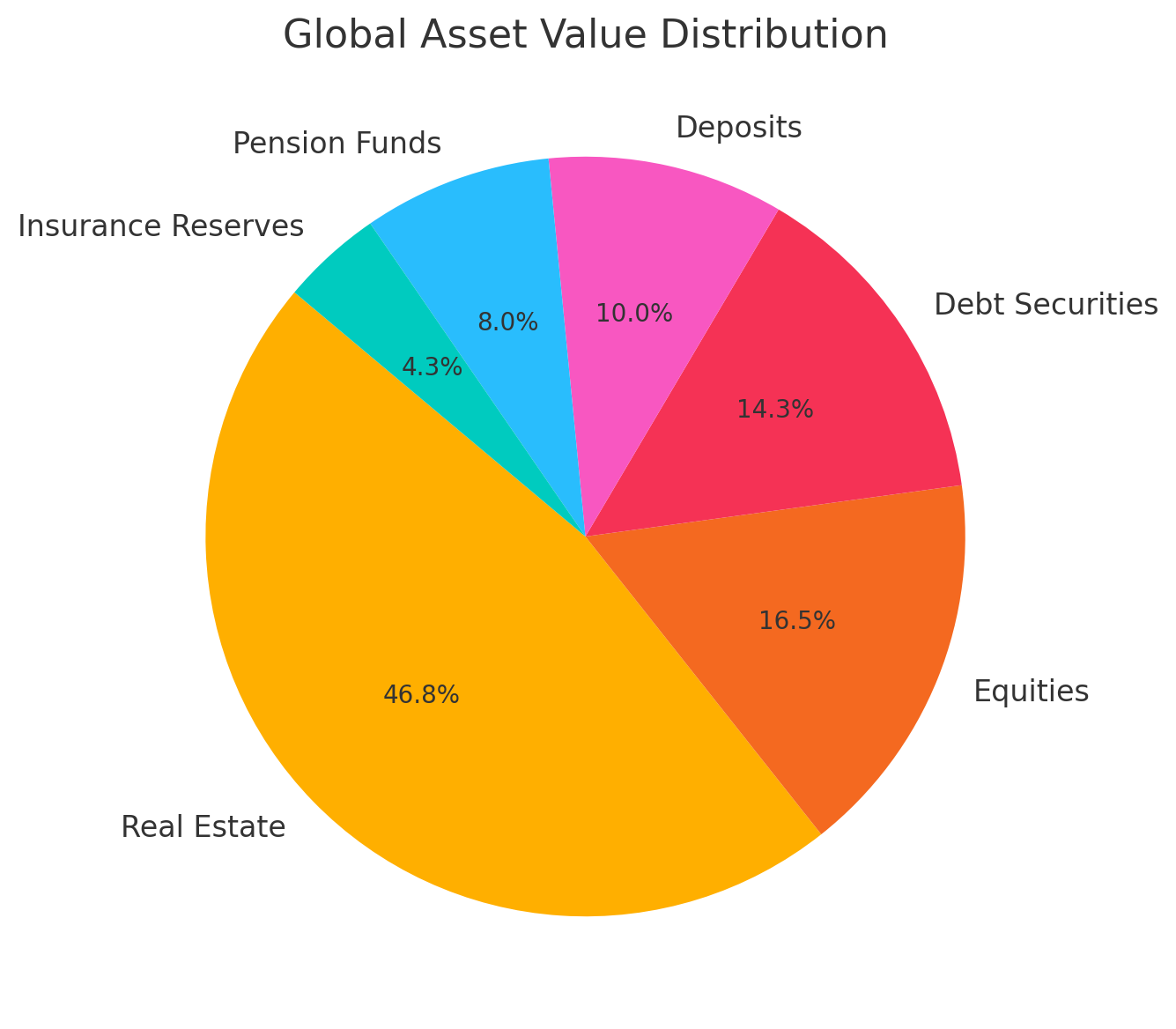

Bitcoin for Saving

Now consider the impact of a new asset class that not only offers better returns than real estate but also provides protection against government-driven inflationary growth of all other assets classes.

We used to have a good method of saving. It was called the gold standard, developed by one of our foremost academics Isaac Newton (also the chap who figured out many of the laws of physics).

Gold was used as a method of accounting because of its relative scarcity compared to all other goods. The harder it is to produce a good, the better it is to account for how much someone has saved. For example, if a gold bar was once worth the equivalent of a mid-range car, after 10 years, to purchase the same car, you would need the original gold bar plus a small gold ring.

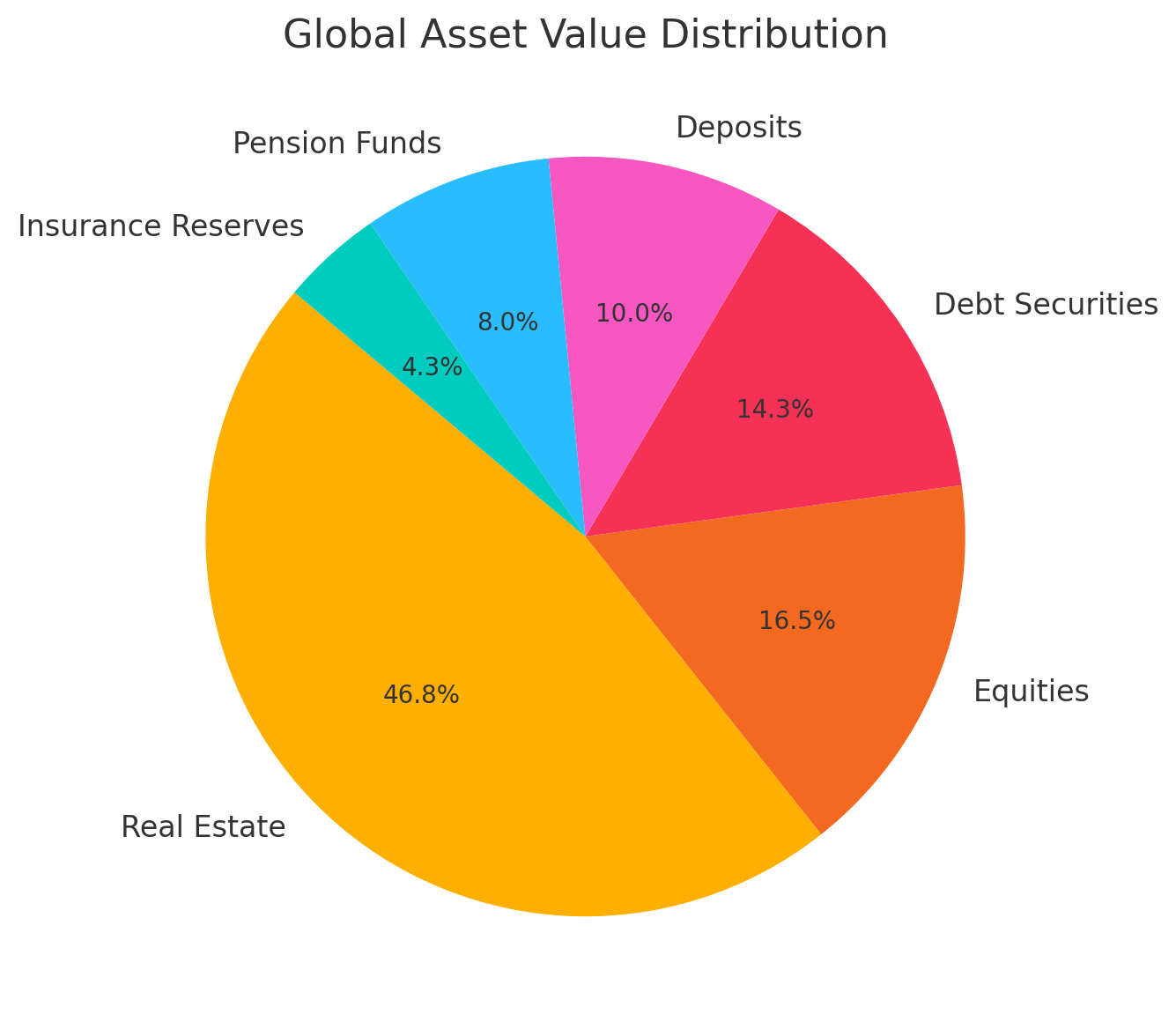

Broad money supply (M3) Jan 1959 – Sep 2023 (Link to chart)

Contrast that to cash ☝️ Assuming an average annual inflation rate of around 7% (which is now conservative!) over the last 10 years, if $100,000 of cash was worth a mid-range car, then after 10 years, you would need approximately $196,715 to purchase the same car, i.e. almost double the price!

Unlike government (fiat) currencies that are subject to inflation and can be devalued by central banks by increasing the money supply, Bitcoin has a fixed supply of 21 million coins. This scarcity makes it a reliable store of value, similar to gold but with the added benefits of digital convenience and security.

Bitcoin's decentralised nature means it isn't controlled by any government or institution, reducing the risk of policy-induced devaluation, while it's inflation rate decreases over time due to its predefined issuance (inflation) schedule.

This means that as the supply of new bitcoins continues to decrease and eventually stops (around 2140), the value of each bitcoin is likely to increase - meaning the prices of goods and services measured in bitcoins should decrease over time.

To invoke the previous example, if a mid-range car costs one bitcoin today, in 10 years, the same car might only cost a fraction of a bitcoin.

As the purchasing power of money (Bitcoin) increases, individuals are incentivised to save and invest their resources more wisely. This natural price deflation reflects the TRUE VALUE of goods and services, encouraging innovation and efficient allocation of resources without the distortions caused by inflationary monetary policies.

Note: Keynesians often say that deflation can hurt businesses (and therefore workers and the economy) because it makes it harder for them to cover their costs. However, as technology improves, production costs go down, allowing companies to stay profitable even if prices are lower. For example, companies like Apple and Samsung have managed to reduce production costs through better supply chain management, automation, and economies of scale.

Bitcoin's Supply

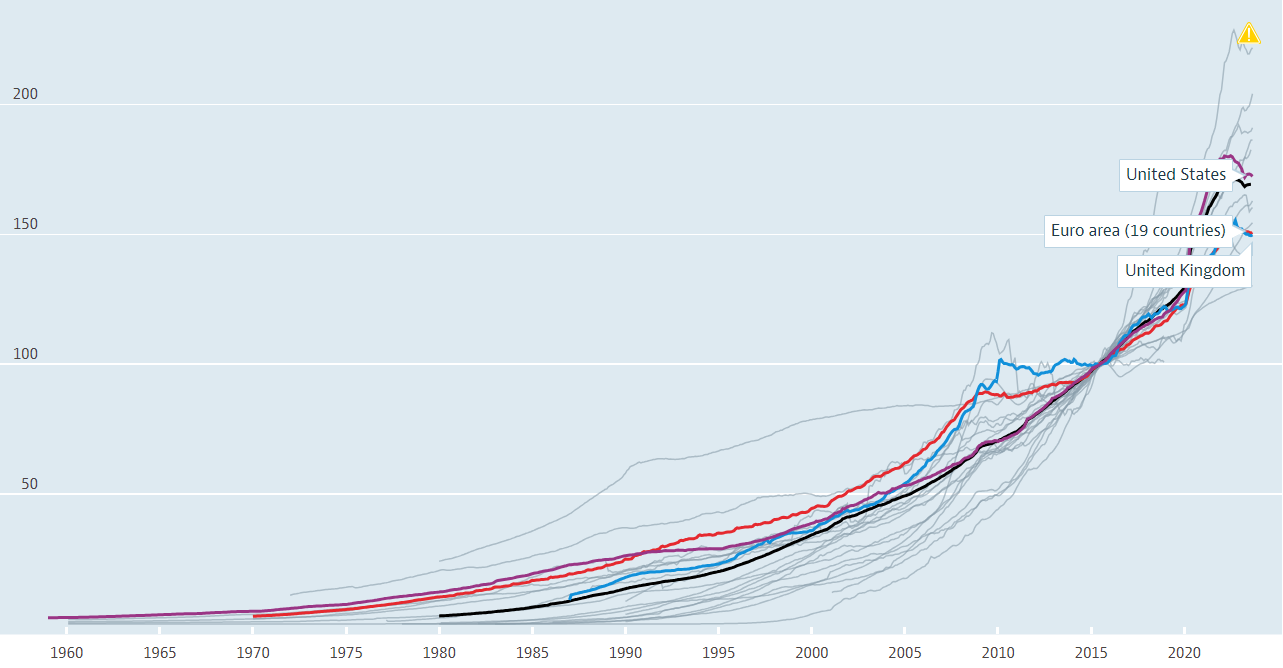

Bitcoin's supply is limited to 21 million, so it's impossible to inflate. Cryptography also makes it nigh on impossible to hack, and there is no single point of failure. That's because nobody owns Bitcoin. No country or central bank. No dictator or political group. It's totally decentralised, and runs across 60,000+ globally distributed nodes at any given time.

There are a bunch of other notable attributes but the most important three are:

1. Limited supply (21m) 2. Extremely difficult to hack (never been achieved in 15-years and getting harder as it grows) 3. Decentralised (not owned by any one entity)

At the moment, the Bitcoin supply is still growing so it has a small inflation rate. However, at some point around 2140, it'll settle at 21,000,000.

This means that Bitcoin will not devalue in comparison to any other product or service, because more of it cannot be made.

However, it's worth noting that Bitcoin is still extremely volatile because of relatively low adoption rates. So if you're interested in buying Bitcoin, make sure you're buying to hold for the long term.

Is Bitcoin Safe?

Bitcoin is built using cryptography and relies on a decentralised network of nodes (people with computers) to keep it secure.

Unless the majority of people agree with any proposed changes to the network, they will be rejected. These changes could be for transactions or regarding the way Bitcoin actually works itself.

Until now, the greatest attack on Bitcoin was in China when the government shut down all mining capacity (a term used to define how Bitcoin is made - to be explained in another post), constituting more than 50% of the whole network. However, due to something called the Difficulty Adjustment (you guessed it, another post), Bitcoin was operating as normal a few weeks later.

Since then, there have been no attacks of a similar size. Bitcoin has been up and running, alive and well since it came online in 2010.

How to get involved in Bitcoin?

Chamath Palihapitiya suggests that everyone hold around 1% of their total wealth in Bitcoin, and hope to god you don't have to use it.

What he means is that if Bitcoin were to grow exponentially, it means the current money system would have failed. I don't see it like that. I see Bitcoin as the best store of value that has ever been created. It's not IF Bitcoin will become a store of value for the long term, it's about WHEN it reaches mass adoption.

As I've been saying ever since reading The Bitcoin Standard, don't be the one without any Bitcoin 😉

--

I'll be posting about various ways to get a hold of Bitcoin in future posts. However, in the meantime, the Bitcoin Newcomers FAQ on r/Bitcoin has some pretty solid options.