Readers who want to know more about the definition of a stock market bubble, should click and read this before reading further: What is a Stock Market Bubble?

So, what is the answer, to the rhetorical question: Are we in a Stock Market Bubble? There can be four ways to answer this question:

Yes

No

I don’t know

I don’t care

My answer is (3) above. I would argue that nobody knows the answer to this question either.

There is always one big truth which serves as the seed for every stock market bubble formation. This has been true for every bubble in financial history. This Big Truth gets blown out of proportion by over enthusiastic market participants, and that leads to a spike in valuations.

What is the ‘big truth’ about the current market environment? This time the big truth is that we will see a repeat of the Roaring Twenties which is a reference to the post pandemic stock market behaviour after the Spanish Flu in 1920. So, the pent up demand will be unlocked once humanity has been vaccinated and its off to the races. Markets being forward looking in nature, they seem to have discounted this in real time. Is this just story telling? How should one factor the Roaring Twenties story in our decision making? The jury is out on this, and personally I don’t think that one should pay any attention to the story telling of the ‘Roaring Twenties’.

My point is that, the Big Truth might not in fact be a big lie, but it won’t play out in the time horizon that most investors expect. As on date, if you’re investing on the basis of this story and with a short-term time horizon, I don’t think you should.

Why do these ‘big truths’ repeatedly get blown out of proportion in the bubble phase? I’ll let Morgan Housel do the talking, and as he has so eloquently pointed out in his book: The Psychology of Money:

An iron rule of finance is that money chases returns to the greatest extent that it can. If an asset has momentum—it’s been moving consistently up for a period of time—it’s not crazy for a group of short-term traders to assume it will keep moving up. Not indefinitely; just for the short period of time they need it to. Momentum attracts short-term traders in a reasonable way. Then it’s off to the races. Bubbles form when the momentum of short-term returns attracts enough money that the makeup of investors shifts from mostly long term to mostly short term. That process feeds on itself. As traders push up short-term returns, they attract even more traders. Before long—and it often doesn’t take long—the dominant market price-setters with the most authority are those with shorter time horizons. Bubbles aren’t so much about valuations rising. That’s just a symptom of something else: time horizons shrinking as more short-term traders enter the playing field.

If we assume for the sake of argument that we are in a bubble, the peculiarities in the current bubble as compared to earlier bubbles are:

The age of the crowd in the current phase differs in a material manner, as compared to the age of the crowd in the calendar year 2000 when we had the tech bubble. In the current phase, most of the participants are below 30 years of age. In the year 2000, they were between 30 and 50 years of age and the average age was closer to 40. This time the average age isn’t more than 30 (that is my guess).

In the year 2000, the crowd had money that they had saved, or some had sold their businesses to participate in the stock market. This time it’s different, the current set of participants have less money and they don’t have as deep a pocket as those in the year 2000. That actually makes the current bubble more fragile and easy to pop.

The current set of participants, just like the cohort in the year 2000, think it’s very easy to make money. Punting is high in stocks that have India’s consumption story as a theme, stocks that have the word platform in their name and in just about anything that exhibits trading momentum. The surprising part is that the fund management universe is also very active in these very names.

Because of the influence of social media, some experts feel that this bull run will last longer than earlier bull runs. What is being missed is the fact that social media is a double edged sword and it can work in reverse as well. So, when there is no one left to buy, the market will ‘clear’ to the downside, it always does.

There is a counter argument that the current bubble is off market, since the real euphoria is seen in places like Bitcoin, Non-Fungible Tokens and crypto related assets. So, even if these off-market bubbles were to burst, there is zero threat of there being any systemic risks. And to state the obvious, at least as on date, we shouldn’t be paying any attention to such off-market bubbles, while thinking about the Stock Market. Personally, I think that this argument has legs.

Why have I answered ‘I don’t know’ to the question: ‘Are we in a Stock Market Bubble?’ The reason is that a bubble is invisible to those inside the bubble. And as a stock market participant and an intermediary, I am definitely inside the bubble if there is one.

And why do I think no one has an answer to the question (Are we in a Stock Market Bubble) either? The reason is that, speculative bubbles are only definitively recognized in hindsight. In other words, even if we are in a bubble, and it does pop or has already popped, we wouldn’t know it for a couple of months after it does. For all we know, the tech bubble might already have popped!

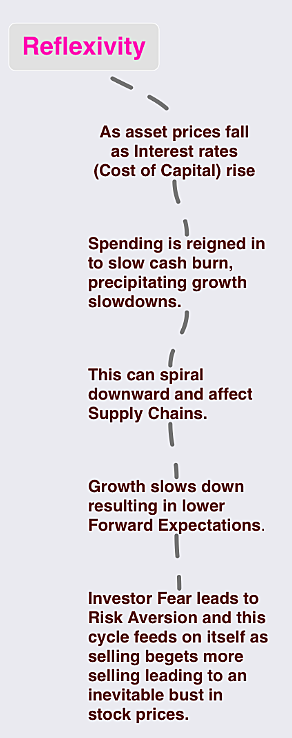

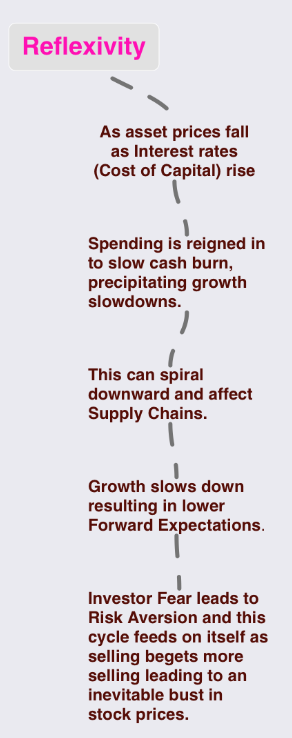

The reason this is so tricky is that the fundamentals will follow price, not the other way around. Why and how can fundamentals follow price? Its called Reflexivity.

George Soros’s reflexivity theory suggests that markets cannot possibly discount the future because they do not merely discount the future but rather also help to shape it. Reflexivity is, in effect, a two-way feedback mechanism in which reality shapes the participants’ thinking and the participants’ thinking shapes reality, in an unending loop.

The image below shows how it works. Please note, the image below is illustrative and I am not saying that this has happened or will happen. What I am saying is that there is no way anybody can read these cycles in real-time. Hence, bubbles can only be called in hindsight. In an up cycle, the image below works in reverse.