When we are buying or selling a stock we are indirectly making a forecast of what we expect the price will be in the future. But, the time horizons for these forecasts, differ from one investor to another. And, time horizons can stretch from a couple of hours to a couple of years.

Irrespective of the time horizon, there is an element of forecasting that is embedded in our decision-making. Our Expectations of what the price will be at the end of our defined time horizon, forms the basis of our forecast.

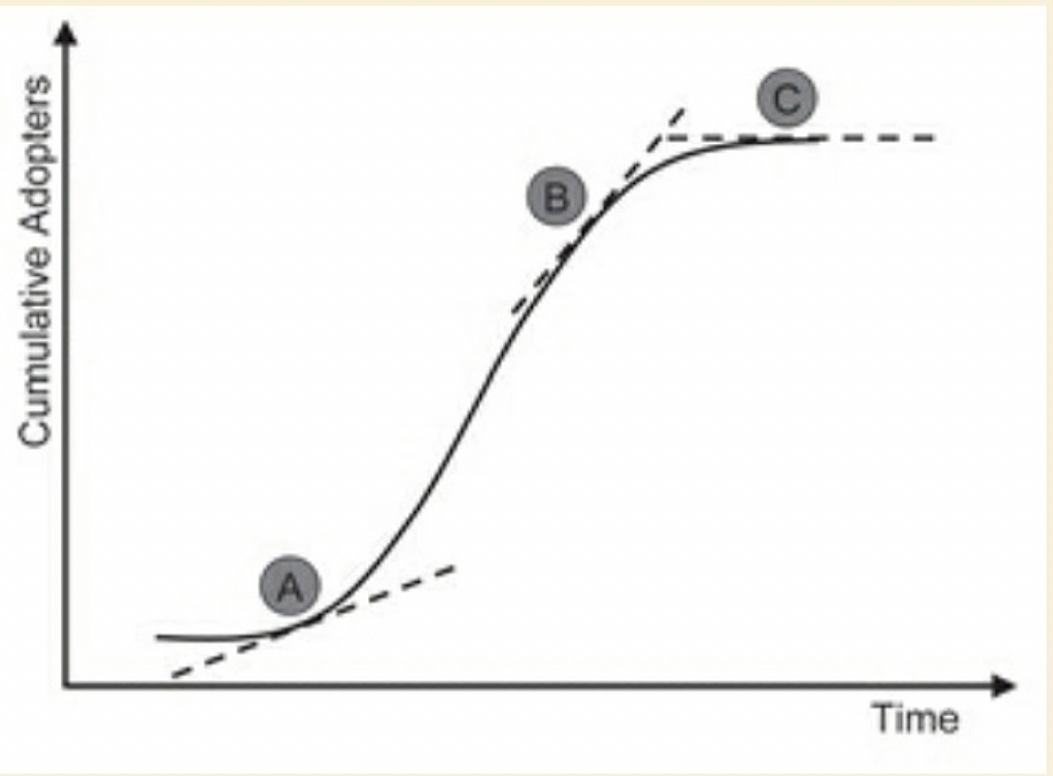

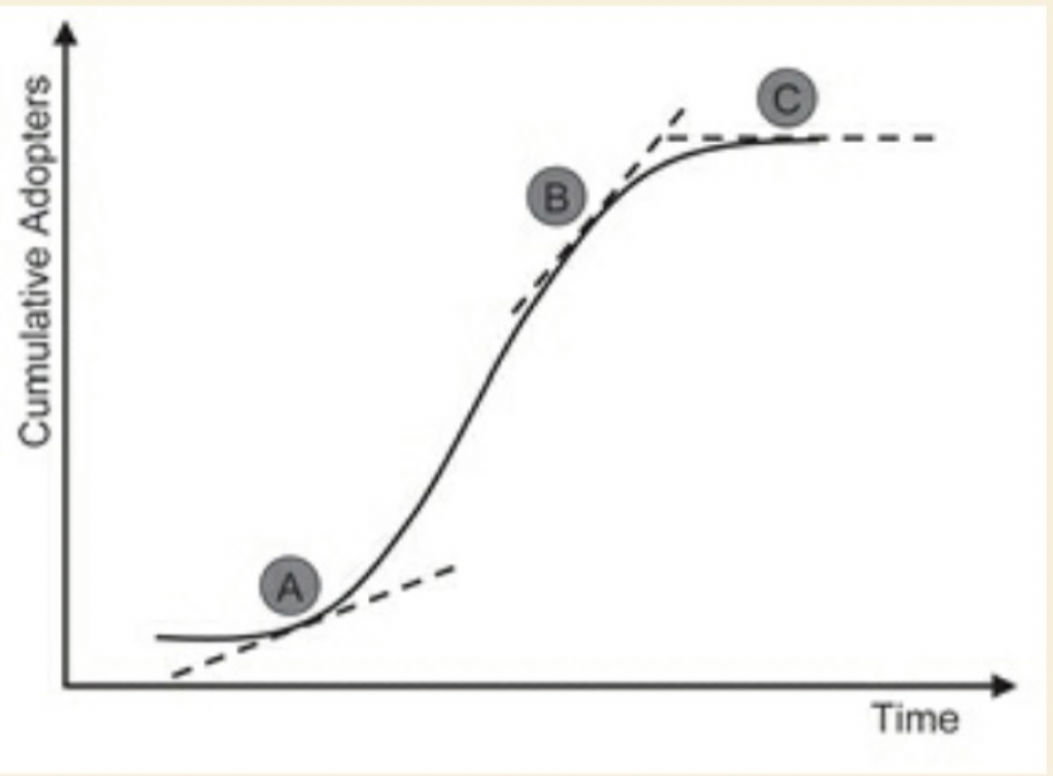

That brings me to the topic of ‘Expectations Investing’. And the easiest way of understanding the concept is with the help of the image of an 'S Curve' shown below:

So at point A, investors do not fully anticipate the growth and economic returns from the business (or the economy), and they extrapolate relatively low growth. The expectations for future financial performance are too low.

Following a period of sustained growth (point B), investors naively extrapolate the recent growth into the indefinite future. Expectations are too high.

Finally, at point C, investors reign in expectations and adjust stock prices to reflect a more realistic outlook.

As investor expectations shift, so do the stock prices of the underlying businesses. Hence:

The obvious goal for an investor is to buy a stock at point A and sell it at point B - avoiding the unpleasant downward expectations revision at the top of the S-curve.

The transition from point A to point B presents opportunities for excess returns (in terms of stock performance) and that the transition from point B to point C often spells poor stock-price performance.

If I were to oversimplify the above concept, we want to buy stocks where the expectations are low, and we want to stay away from stocks that are pregnant with expectations. The reason is that, low investor expectations translates to low stock prices and a better risk-reward. The inverse is equally true.

What does all of the above say about investor expectations as on date? After a sharp run up, expectations aren’t bearish or low. Over the short-term, the upcoming quarterly earnings season will tell us if investor expectations have gotten ahead of themselves or if the converse, is in fact, what has happened.

If earnings beat expectations, stocks will rise. As a result, over the short-term, the earnings season will decide individual stock price volatility. It might just make sense to wait for an opportune time to commit capital. That doesn’t mean one should just sell one’s portfolio and run away. Doing nothing seems to be the best thing to do.